Priorities

EU ETS/ CBAM

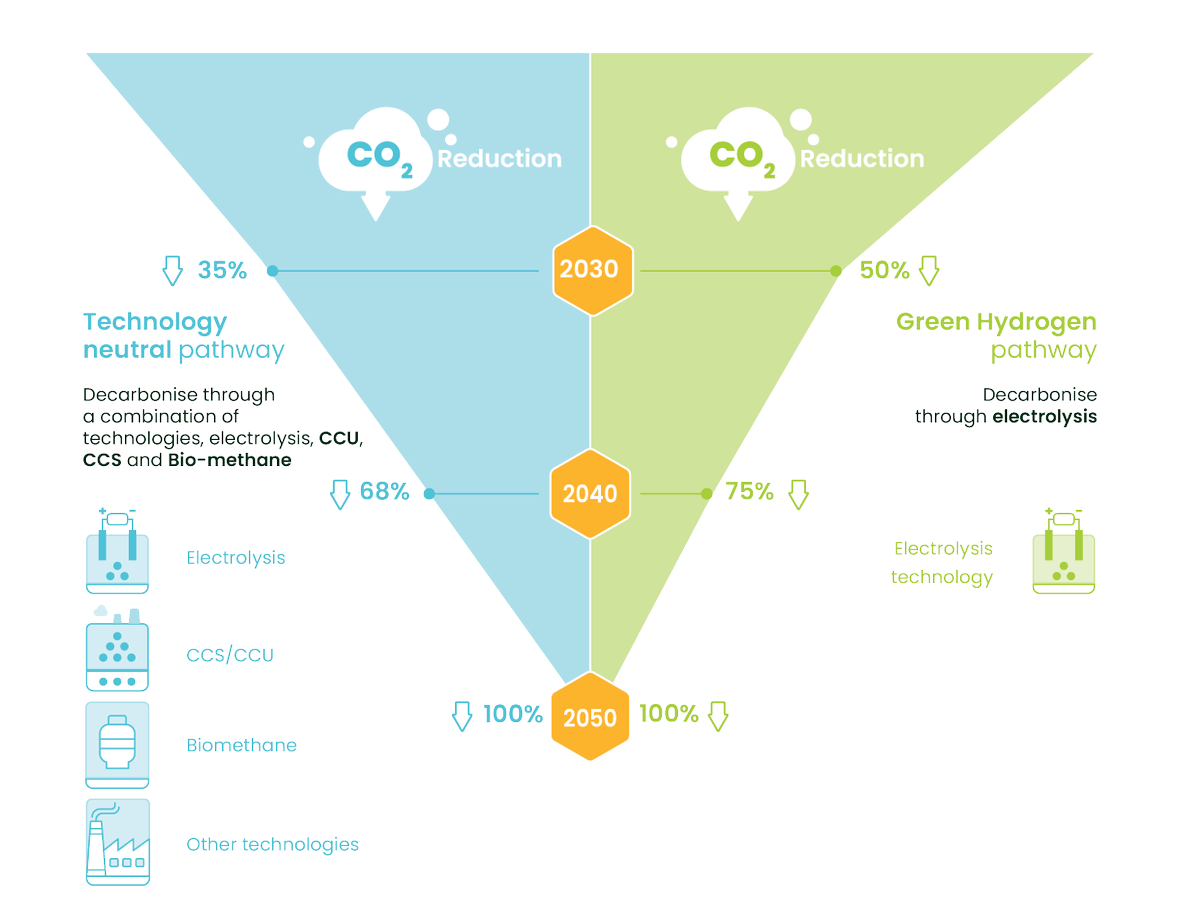

Clean Planet for All

Farming & Air Quality

By the numbers

The Fertilizer Industry in Europe

9.8

BILLION EURO TURNOVER

66.2

MILLION EURO INVESTED IN R&D BY OUR MEMBERS

75.000

EMPLOYEES

1.4

BILLION EURO ANNUAL INVESTMENT

From Twitter

@FertilizersEuro

. @MncaAndres highlighted at the CleanTransitionDialogue with the @EU_Commission Commission, the EU #fertilizer industry's needs for a successful transition:

-Renewable energy

-Large-scale project funding

-#CBAM review

-Stable regulations

-Incentives for low-carbon products.

The Clean Transition Dialogue with @EU_Commission EVP @MarosSefcovic was a great opportunity to discuss the future of the EU fertilizer sector and how it can continue playing a critical role in ensuring #foodsecurity, decarbonizing food production & enabling the hydrogen economy.…

The Decarbonisation Roadmap of the EU #fertilizer sector aims for a climate-neutral industry by 2050. It is a bold but essential step to meet the #EUGreenDeal targets, ensure food security, strategic autonomy & sustainable food production in EU. https://bit.ly/47PDlgl

"By enriching the soil with nutrients, fertilizers increase agriculture productivity, ensuring nutritious and healthy food for all." #EUYoungFarmers

ℹ️ More info on @FertilizersEuro ➡️ https://shorturl.at/mWZ46

"Through the development of tools and innovative solutions, European fertilizer producers empower farmers to produce more with less." #EUYoungFarmers

ℹ️ More info on @FertilizersEuro ➡️ https://shorturl.at/juvzJ

EU Fertilizer industry embraces the EU’s

ambition to be climate neutral by 2050. The Decarbonisation Roadmap unveiled today sets an ambitious journey. With the appropriate legislative framework, investment landscape, & collaborative efforts we will ensure EU's food security &…

Our association

The association communicates with a wide variety of institutions, legislators, stakeholders and members of the public who seek information on fertilizer technology and topics relating to today’s agricultural, environmental and economic challenges.